See a Sample Financial Plan: Our BluePages Planning Process

By Russell Holcombe, MTx, CFP®

After decades of experience working with clients in various stages of the wealth-building process, it became clear that the industry-standard approach for creating a financial plan was fundamentally flawed. It was missing the most important component of life: change. Nothing stays constant, and the assumptions built into most financial planning software don’t perform well in fluid situations. That’s why we at Holcombe Financial decided it was time to create our own financial planning software, BluePages.

At the beginning of my career, I learned by watching my father. He was a specialist in financial triage and helped people manage precarious financial situations. Some of these predicaments were self-inflicted (like unaffordable second homes and overspending), but many were faultless (like the disability or death of a spouse, divorce, or a job loss). Regardless of why, the ability of a family to survive financial trauma was based on a few very easy-to-calculate metrics. Understanding these metrics helps guide good financial decision-making.

A financial plan needs to not only adapt, but it also needs to evolve as our clients’ lives unfold, and also be straightforward and easy to understand. We thought it best to give you an overview of what to expect before you commit to letting us help you manage your financial future.

Here’s what a BluePages sample financial plan looks like and why it’s different from other planning models on the market.

The Building Blocks of a Financial Plan

We officially began building BluePages in 2012. At that time, financial decision-making mostly consisted of projections of future wealth through Monte Carlo simulations and assumptions about returns, inflation, and interest rates. All of these are unpredictable within a single year, let alone 30 years. It was crystal-ball economics. None of the day-to-day factors that affect the average family (career choices, housing decisions, life and disability decisions, compensation packages, etc.) were included. The current market software assumed you would be the same person forever, and completely neglected the age-old fact that change is inevitable.

We didn’t dive right into building our own financial software right away, though. We spent time doing our due diligence by creating a hypothetical financial scenario as a guinea pig to test the most popular financial planning software at the time. Our thought process was that the same set of inputs should theoretically lead to similar outcomes, regardless of the software used.

Sadly, the implicit assumptions that each plan used led to vastly different outcomes. Depending on which software an advisor used, the financial forecast would be completely different.

The current versions of financial planning software are prettier now, synched with investment accounts, and they are getting better overall. But so many advisors still use Microsoft Excel to supplement the current financial planning products because it requires someone with experience to interpret the results. You have to know when the software is out over its skis.

After seeing the results of the BluePages with hundreds of clients over the past decade, we knew the challenge of building our own software was worth it. The ability to help clients approach a crossroads and understand the financial consequences of each outcome is the purpose of financial planning. A successful life is the accumulation of successful small decisions, and successful small decisions come from a plan that helps you address real-life challenges and evolves as you do.

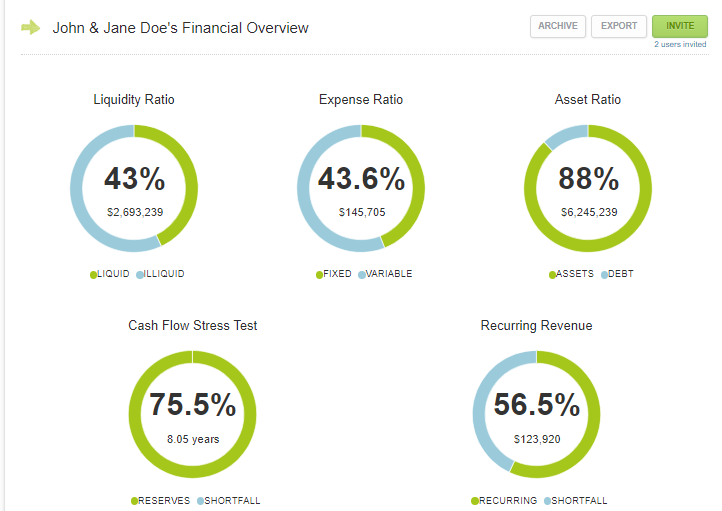

The BluePages Financial Dashboard

The BluePages Financial Dashboard is a quick tool to assess the financial strengths and weaknesses of your current financial situation. At the end of the day, your ability to survive financial trauma, retire, or take advantage of financial opportunities will be based on the strength of these metrics.

We analyze five important ratios:

Liquidity Ratio

This is the most important metric on the dashboard and is often overlooked by many young families as they build wealth. Your ability to change your financial circumstances in the short term will be dictated by your liquidity ratio; a common mistake we see young couples make is over-saving in 401(k), HSA, or 529 plans. We are big fans of these savings options, but they don’t help when there is an interruption in cash flow.

An asset that is liquid is one that can be available in 24 hours if the need arises. Cash and after-tax investment accounts check the “yes” box. Homes, retirement plans, and 529 plans are wonderful vehicles but can’t help in a financial emergency. If you had the best financial opportunity of a lifetime and/or a financial emergency, how much money could you get in 24 hours? It is a powerful test of financial strength.

Cash Flow Stress Test

The Cash Flow Stress Test measures how long you can survive on after-tax liquid assets without having to change your lifestyle. Imagine if you lost your job…the Cash Flow Stress Test gauges the length of time you have before you need to get anxious. Hopefully measured in years and not months, your financial strength is about options. If you only have a few months of savings, you may have to take the first job offered versus waiting for the best job offered.

Expense Ratio

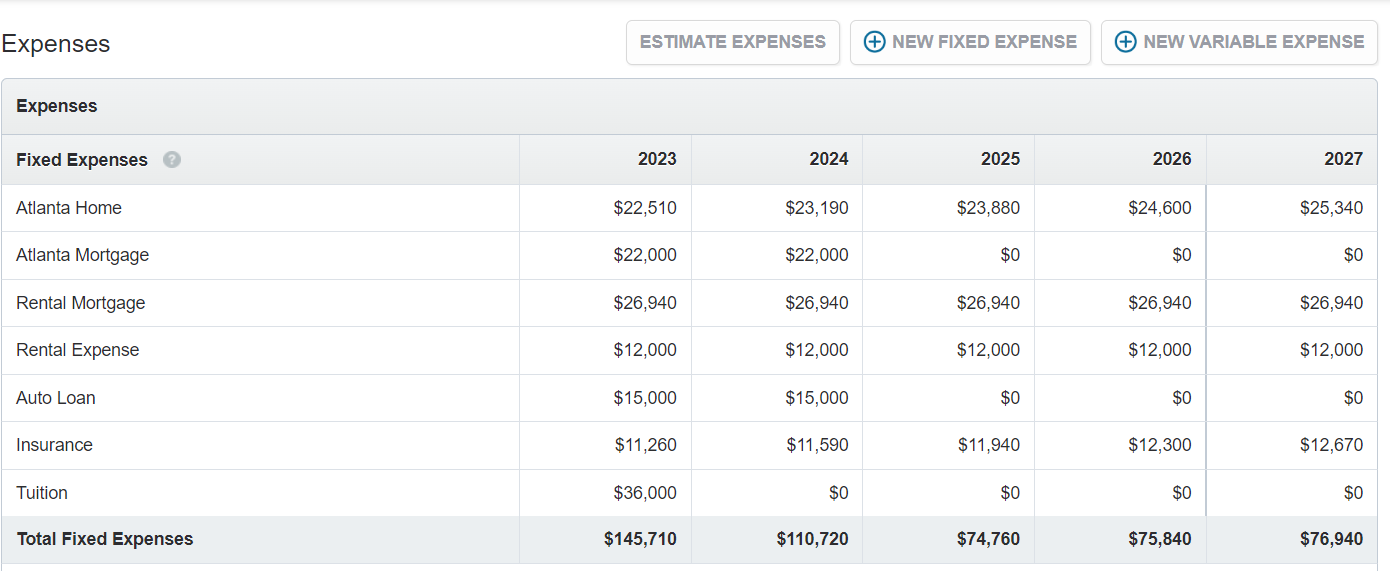

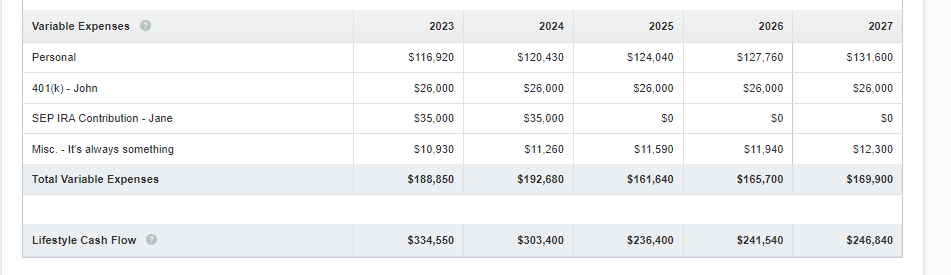

We are categorizing the family budget into two categories based on the following question: “If something required you to change your lifestyle, what could you adjust in 24 hours?” Your financial flexibility is conditioned on this metric. If you lose your job, your mortgage is still due, and your property taxes are fixed, but you can spend less on the American Express card, stop the 401(k), and cut back on charitable donations. We break expenses down into “fixed” and “variable” and get concerned if “fixed” exceeds 50% of Lifestyle Cash Flow.

Recurring Revenue

This is a measure of your progress toward financial independence. The numerator is income you generate without effort in retirement like Social Security, pensions, and rental income. The denominator is Family Overhead, which removes expenses that will cease to exist in retirement, such as tuition, 401(k), and hopefully mortgage debt. When the number exceeds 100%, work becomes optional.

Asset Ratio

The asset ratio is helping you understand your leverage. When you review your balance sheet, how much of it is yours, and how much of it has corresponding debt? This is a secondary ratio, which is why it is lower on the dashboard. Leverage can cause other metrics to be higher, but by itself, it does not impact financial strength directly. If debt is over 50% of assets, it requires additional questions of the stress test.

Statement of Cash Flow

When we work on a financial plan, the balance sheet is important. I don’t want to discount its usefulness in assessing financial stability. Are assets liquid or illiquid? How much cash is available? How much leverage exists, etc.? But far too much time is spent studying the balance sheet and not enough time is spent on understanding the cash flow statement. The linchpin of every financial plan is the Statement of Cash Flow. This is why people are wealthy; it is the blocking and tackling of success.

The underlying purpose behind all financial planning exercises is to stress test the cash flow statement to uncover hidden risks. Retirement is a byproduct of successful planning. Some sample scenarios below are all based on the cash flow statement:

- Can my investment accounts generate enough income so I can retire? To answer this question affirmatively, the earnings from the investment account on a before-tax basis plus the income from Social Security, pensions, rental property, etc., should exceed Family Overhead (Lifestyle Cash Flow + Income Tax). If it does not, the next step is to figure out how to cover the shortfall.

- Does my spouse have enough life or disability insurance? Answering this question requires adjusting the cash flow to test for shortfalls in Family Overhead. If there is not enough income to cover Family Overhead, the shortfall must come from somewhere. How much is that shortfall, and how do you plan to fund it?

- Should I max out my 401(k) or HSA? While maxing out all tax-deferred accounts is helpful from a tax perspective, how much is left over to build up liquidity, pay down student loans, or reduce mortgage debt?

This is just a short list of scenarios that a good financial planner will walk you through, and all are dependent on a detailed understanding of your Statement of Cash Flow.

Start With Income

In the BluePages, we create a five-year pro forma statement for our clients based on income expectations in the foreseeable future. Planning requires assumptions, but anything in this section should have more than a reasonable probability of occurring. Projections create risk, and the longer the time period, the more unreliable the output. Going out beyond five years or using Monte Carlo simulations are too hypothetical to be useful. Real data with likely outcomes is the only way to make educated decisions.

Know Your Overhead

Income is easy. Everyone knows how much they make. Tracking expenses is hard, and the menagerie of apps that claim to do it better just highlights how challenging it can be. We like to think of each family like a small business. Imagine yourself as the CEO and CFO. A big part of being a CFO is understanding the cash flow. Businesses spend a great deal of time trying to grow revenue, and those that excel make sure that they manage for a profit.

As we discussed on the dashboard, expenses come in two forms: fixed and variable. I wish there was an easy way to track expenses. There is a tendency to hyper-categorize them. People feel like the more data they have, the better they know their expenses. The struggle with more is it creates complexity. And the more complex the data set, the harder it will be to see the big picture. As financial planners, we prefer broad categories that encapsulate the behavior. For example, personal expenses include everything you love to do and it normally shows up on the credit card each month. Add up 12 months of credit card statements and you’ll have a good feel for how much your lifestyle costs per year.

It is important to note that a variable expense does not necessarily mean it can go to zero. You still have to eat. It just means you can choose to eat at home versus at a restaurant. You can decide to stop your 401(k) contribution at any time. Vacations can wait, and you can make your charitable contributions next year. A variable expense is a flexible expense. Anytime the fixed expenses exceed 50% of overall Lifestyle Cash Flow, it is a cautionary warning in our financial planning reviews.

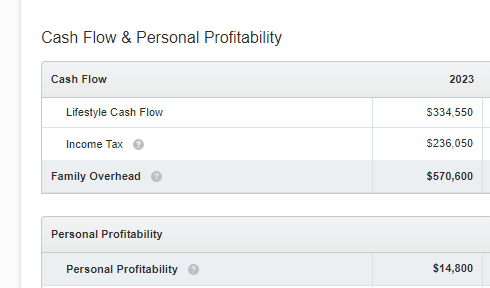

The purpose of the exercise is to find Lifestyle Cash Flow. Every family should know this number. It can be simply defined as the sum total of all the money that is expected to be spent in one year. Whether it be payments to a mortgage company or savings in the 401(k), it has to be funded from income (or the balance sheet if there is not enough income). How much does it take to do the things we love? In the example above, it is $334,550 this year.

The final piece to the cash flow puzzle is income tax, which, sadly, consumes between 30-40% of the family budget every year.

The net result of the Statement of Cash Flow is Personal Profitability. Families that build wealth save after-tax wealth. We consider breakeven to be roughly 10% of income, and a high achiever is able to save more than 15% after-tax each year.

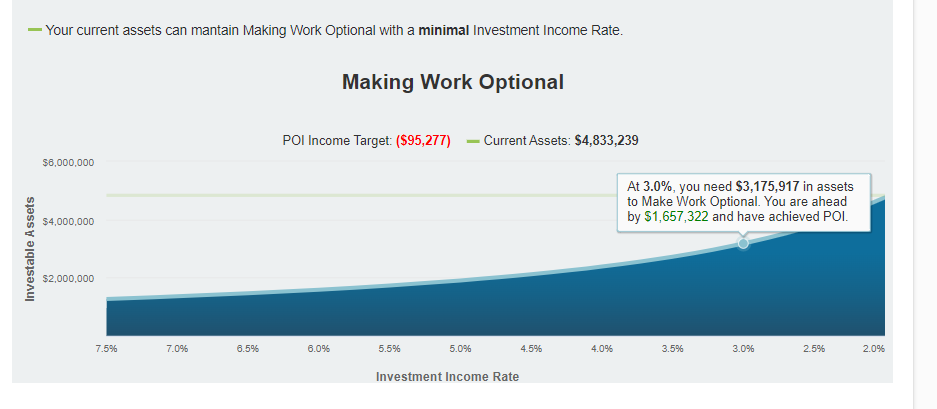

The Goal: Making Work Optional

The moment you can retire with zero risk is when you have secured a passive income stream that pays 100% of your Family Overhead. I don’t like the word retirement. I prefer Making Work Optional. It is the point where you are financially independent and fully in charge of your own destiny. Thankfully, it is not a difficult calculation.

Your Lifestyle Cash Flow less expenses that will stop naturally: your student debt will be paid off, the kids will graduate, your 401(k) and HSA cease when you stop working. Subtracting expenses that will go away naturally brings us to your Point of Independence Cash Flow. Most people don’t realize how much less your Family Overhead becomes once you clear these milestones.

This is a road map, but it requires an understanding of investment strategy and a thorough assessment of risk to execute. Many people’s financial independence was dented last year because they did not understand the risk they were taking. This is why a professional is so important. It is hard to fix a broken balance sheet and replace 20 years of hard-earned wealth with only 3 years before retirement. It’s important to know if you’re on the right track—and that is why we built BluePages.

Experience the BluePages Difference

At Holcombe Financial, we are dedicated to helping our clients Make Work Optional. And our BluePages software is what we use to make it happen. If you’re ready to experience true comprehensive financial planning and the BluePages difference, we would love to hear from you! Schedule a no-obligation introductory meeting to see how we can help by calling us at (404) 257-3317 or emailing hello@holcombefinancial.com.

About Russell

Russell (Rusty) Holcombe is the CEO and strategist at Holcombe Financial, a financial advisory firm serving entrepreneurs and corporate executives and managers. With over 25 years of experience, Rusty spends his days leading Holcombe Financial (a firm his father founded) and providing financial services that help his clients grow and protect their wealth so they can experience financial independence. Rusty is the author of You Should Only Have to Get Rich Once, which has won multiple awards, and created Holcombe Financial’s proprietary financial planning software, which helps clients make smarter financial decisions.

Rusty earned a bachelor’s degree in business administration with a focus in finance and real estate from Southern Methodist University and a master’s degree in taxation from Georgia State University. He is also a CERTIFIED FINANCIAL PLANNER™ professional. In his free time, Rusty and his wife, Regina, tend to their personal farm and grow their own food. You can often find him pursuing his hobby of long-distance running. To learn more about Rusty, connect with him on LinkedIn. You can also watch his latest webinar on investing.